As private markets mature and deal access becomes more competitive, investors and fund managers are increasingly turning to Special Purpose Vehicles (SPVs) as a flexible, efficient way to structure investments. From angel syndicates and venture capital to private credit and secondaries, SPVs have become a core building block of modern private investing.

In this article, we’ll break down why SPVs are used, how they work in practice, and why platforms like Allocations are making SPVs faster, safer, and easier to manage at scale.

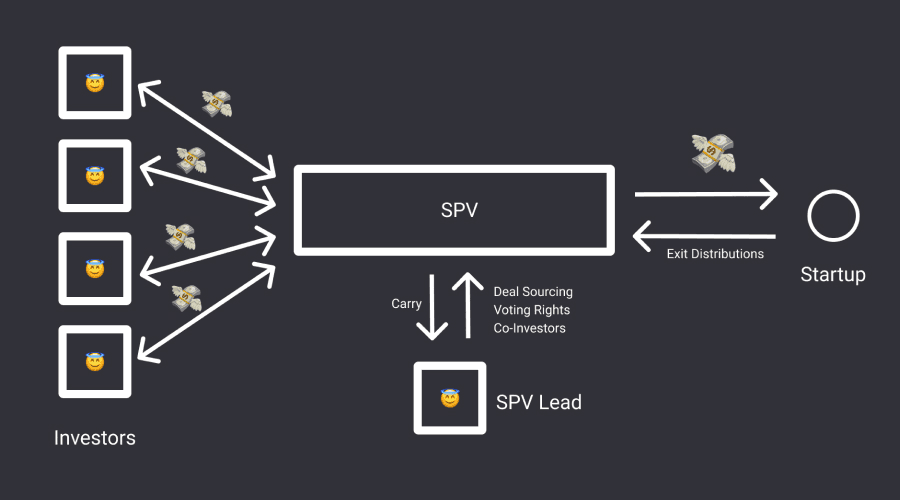

What Is an SPV?

A Special Purpose Vehicle (SPV) is a standalone legal entity—typically an LLC or LP—created to hold a single investment or a narrowly defined set of assets.

Instead of multiple investors investing directly into a startup or asset, they pool their capital into the SPV. The SPV then makes the investment as one line item on the cap table.

At a high level:

Investors → invest into the SPV

SPV → invests into the company or asset

Returns → flow back to investors through the SPV

This structure may seem simple, but it unlocks several powerful advantages.

1. Cap Table Simplification for Founders

One of the most common reasons SPVs exist is to simplify cap tables.

Without an SPV, a startup raising capital from 20–100 angel investors would have:

Dozens of names on the cap table

Complex voting and consent mechanics

Higher legal overhead for future rounds

With an SPV:

The company sees one investor (the SPV)

Governance is cleaner and easier to manage

Future institutional investors are more comfortable

From a founder’s perspective, SPVs are often a non-negotiable requirement for accepting angel or syndicate capital.

2. Access to Deals Without Running a Full Fund

Traditional venture capital and private equity funds are powerful structures—but they are not always practical. Launching a fund typically requires multi-year investor commitments, extensive legal and regulatory setup, and fund-level economics that may not suit every opportunity. According to industry estimates, setting up a traditional VC fund can take 6–12 months and cost six figures in legal and compliance expenses before a single dollar is invested.

SPVs offer a significantly lighter alternative.

Rather than committing to a blind pool of capital, SPVs allow deal leads and syndicate managers to raise capital one transaction at a time. This structure is particularly valuable in competitive private markets, where high-quality opportunities often arise unpredictably and require fast execution. Instead of waiting for fund approval cycles or reserving capital across dozens of potential investments, managers can form an SPV only when a deal meets their conviction threshold.

This model has fueled the rise of angel syndicates and solo capital allocators. Over the last decade, deal-by-deal investing has grown rapidly, especially in early-stage venture, where many of today’s most active investors operate without a formal fund. SPVs allow these investors to remain flexible, opportunistic, and aligned with their networks—without taking on the operational burden of becoming a regulated fund manager.

In short, SPVs lower the barrier to entry for accessing private deals while preserving institutional-grade structure.

3. Better Alignment Between Investors and Deals

One of the fundamental drawbacks of traditional fund structures is information asymmetry at the time of commitment. Investors commit capital first and learn the specifics of portfolio construction later. While this model works well for diversified exposure, it can dilute alignment for investors who prefer precision and transparency.

SPVs reverse this dynamic.

Each SPV is created for a single, clearly defined investment—a specific company, asset, or transaction. Investors know exactly what they are backing, at what valuation, under which terms, and with what risk profile. This clarity enables informed decision-making and attracts investors who want intentional exposure rather than broad, pooled risk.

From a performance perspective, SPVs also change how success is measured. Instead of evaluating outcomes across a blended fund portfolio, returns are assessed deal by deal. This creates stronger accountability for deal leads and clearer attribution for investors. In practice, this transparency often leads to higher trust, stronger long-term relationships, and more repeat participation in future SPVs.

As private markets mature, sophisticated investors increasingly favor this level of granularity—and SPVs are the structure that enables it.

4. Risk Isolation and Liability Protection

Risk management is a core reason SPVs exist.

Because each SPV is a standalone legal entity, it creates structural isolation between investments. If an individual deal underperforms or encounters legal, regulatory, or operational issues, those risks are contained within that specific vehicle. Other SPVs—and other investments—remain unaffected.

This isolation is particularly important in asset classes where downside risk is asymmetric. Early-stage startups, private credit, international transactions, and regulated industries all carry unique exposure profiles. By separating each investment into its own entity, investors limit their liability strictly to the capital committed to that SPV.

From a legal standpoint, this separation acts as a firewall. Investors are shielded from cross-claim exposure, and managers reduce the risk that a single problematic deal could jeopardize an entire investment program. For this reason, SPVs have become standard practice in professional private investing, even among large institutions.

5. Flexible Economics and Custom Deal Terms

Another key advantage of SPVs is economic flexibility.

Unlike funds, which typically apply uniform management fees and carry across all investments, SPVs allow economics to be tailored on a deal-by-deal basis. This is essential in real-world private markets, where not all opportunities are created equal.

For example, a highly competitive secondary transaction may justify lower fees in exchange for speed and access, while a proprietary early-stage deal may include higher carry to reflect sourcing and value-add. SPVs can also accommodate side letters, strategic investor terms, or bespoke waterfalls that would be cumbersome—or impossible—to implement at the fund level.

This flexibility is especially important for lead investors who bring more than capital. Operators, domain experts, and strategic angels often contribute sourcing, diligence, or post-investment support. SPVs allow these contributions to be reflected economically, aligning incentives without overcomplicating the structure.

Modern platforms like Allocations standardize these mechanics, ensuring that custom terms remain clean, auditable, and easy to administer.

6. Efficient Tax and Reporting Structure

From a tax perspective, most SPVs are structured as pass-through entities, meaning profits and losses flow directly to investors rather than being taxed at the entity level. This avoids double taxation and aligns with how most private market investors expect returns to be treated.

However, while the tax treatment is straightforward in theory, execution has historically been complex. Managing individual K-1s, capital accounts, distributions, and ongoing reporting across dozens—or hundreds—of investors is operationally demanding.

This is where modern SPV infrastructure has changed the equation.

Instead of manual spreadsheets and fragmented service providers, today’s SPV platforms automate allocations, generate tax-ready reporting, and provide investors with centralized dashboards. As a result, SPVs are no longer reserved only for large checks. They are now viable for repeat, smaller investments, enabling broader participation without increasing administrative burden.

7. Enabling Secondary and Late-Stage Transactions

SPVs play a critical role in unlocking access to secondary and late-stage private deals.

These transactions often involve time-sensitive opportunities, multiple buyers pooling capital, and sellers who demand clean execution. Founders, early employees, and early investors increasingly seek liquidity before IPO or acquisition, driving rapid growth in the private secondary market—now estimated to exceed $100 billion annually.

SPVs are uniquely suited to this environment. They allow capital to be aggregated quickly, shares to be acquired efficiently, and ownership to be consolidated under a single entity. Without SPVs, many of these deals would be inaccessible to smaller investors or impractical to execute within tight timelines.

In effect, SPVs democratize access to late-stage private market liquidity while preserving institutional standards.

8. Operational Simplicity at Scale

Historically, SPVs were viewed as cumbersome. Formation was slow, banking was fragmented, and investor onboarding was manual. These frictions limited SPVs to niche use cases.

That reality has changed.

Today, platforms like Allocations provide end-to-end SPV infrastructure: entity formation, digital KYC/AML onboarding, integrated banking, compliance workflows, and automated distributions—all within a single system.

This operational simplicity has transformed SPVs from a workaround into core private-market infrastructure. Managers can now launch and manage multiple SPVs in parallel without scaling operational overhead, making the structure suitable not just for one-off deals, but for repeatable investment programs.

Final Thoughts

SPVs are no longer a tactical shortcut—they are a strategic investment tool.

They offer precision where funds offer scale, flexibility where funds impose uniformity, and transparency where traditional structures rely on trust over visibility. By simplifying access, aligning incentives, isolating risk, and reducing operational friction, SPVs have become the preferred structure for modern private investing.

As private markets continue to expand and specialize, SPVs—powered by platforms like Allocations, are increasingly the default way sophisticated investors participate in high-quality private opportunities.

SPVs

Read more

SPVs

Read more

Company

Read more

SPVs

Read more

SPVs

Read more

Fund Manager

Read more

Fund Manager

Read more

Analytics

Read more

Analytics

Read more

Fund Manager

Read more

Fund Manager

Read more

Fund Manager

Read more

Company

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

Fund Manager

Read more

Fund Manager

Read more

Investor Spotlight

Read more

SPVs

Read more

Market Trends

Read more

Company

Read more

Analytics

Read more

Market Trends

Read more

Market Trends

Read more

Products

Read more

Fund Manager

Read more

Fund Manager

Read more

Fund Manager

Read more

Analytics

Read more

Market Trends

Read more

Fund Manager

Read more

Analytics

Read more

Analytics

Read more

Investor Spotlight

Read more

Analytics

Read more